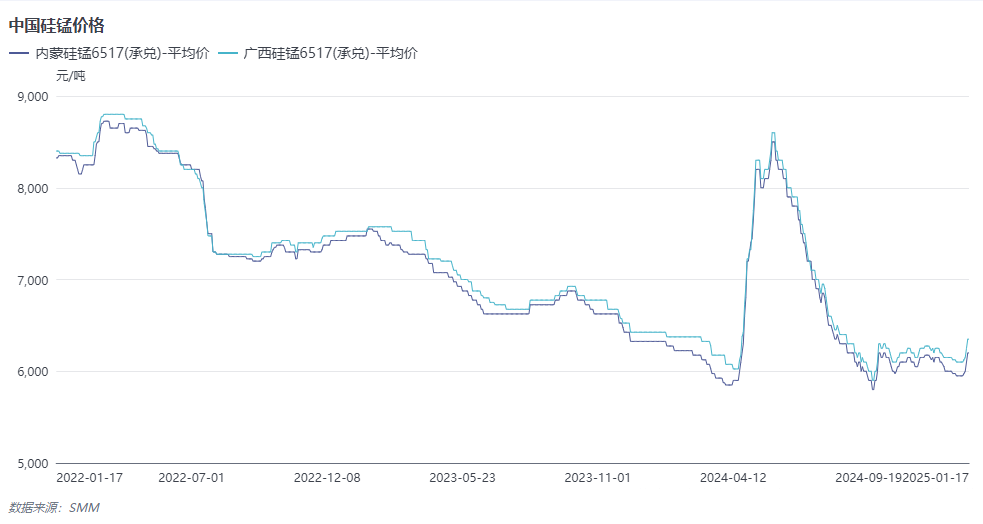

I. Price Aspect:

The annual average price of SiMn alloy 65/17 in Inner Mongolia in 2024 was 6,541.32 yuan/mt, down 5.07% YoY; the annual average price in Guangxi was 6,660.74 yuan/mt, down 4.69% YoY.

From the quarterly price review:

2024 Q1: Supply side, the reduction caused by power rationing or maintenance in north China recovered, but SiMn alloy production fell short of expectations. However, due to relatively high social inventory levels, SiMn alloy supply remained sufficient. Demand side, as steel mills had sufficient stockpiles of SiMn alloy and resumed production at a slow pace after the holiday, downstream steel mills showed weak demand and low enthusiasm for SiMn alloy procurement, leading to a decline in SiMn alloy prices in Q1.

2024 Q2: Influenced by news of disruptions in mine shipments, miners showed strong sentiment to stand firm on quotes, and spot ore prices rose significantly. With strong cost support, SiMn alloy spot prices surged rapidly. Supply side, SiMn alloy plants with pre-stocked manganese ore resumed production, and SiMn alloy production increased month by month. Demand side, downstream steel mills entered the traditional "Golden March and Silver April" peak demand season, boosting their enthusiasm for SiMn alloy procurement. Supported by cost-driven factors and recovering demand from downstream steel mills, SiMn alloy spot prices continued to rise.

2024 Q3: Supply side, due to high costs and severe production losses, many SiMn alloy plants shut down furnaces for maintenance, reducing production. However, combined with previous inventory, SiMn alloy supply remained at a high level. Demand side, downstream steel mills showed weak willingness to purchase SiMn alloy, and the market's oversupply situation persisted, causing SiMn alloy spot prices to continue declining.

2024 Q4: Supply side, ore prices stabilized, reducing costs and easing production pressure for SiMn alloy plants, leading to an increase in operating rates. SiMn alloy plants mainly fulfilled long-term contracts, showing weak willingness to sell spot orders at low prices. Demand side, downstream steel mills had pre-holiday stockpiling needs, focusing on just-in-time procurement of SiMn alloy. The tug-of-war between sellers and buyers led to spot prices fluctuating downward.

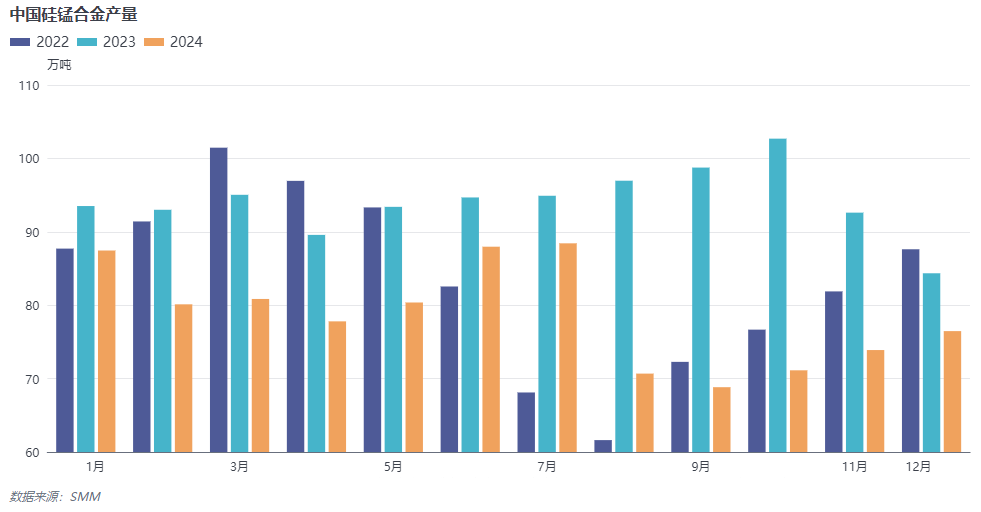

II. Supply Aspect:

According to SMM data, China's total SiMn alloy production in 2024 was approximately 9.438 million mt (including high-silicon SiMn alloy), down 16% YoY compared to 2023. The significant decline in overall production was mainly due to two factors: first, SiMn alloy capacity surplus and lower-than-expected end-user steel consumption kept SiMn alloy in an oversupply situation. Second, the sharp rise in ore prices led to high production costs for SiMn alloy, causing severe production losses and widespread shutdowns for maintenance, further reducing overall SiMn alloy production.

III. Demand Aspect:

SiMn alloy's downstream demand is primarily for rebar production. In 2024, crude steel production decreased YoY compared to 2023, and steel mills reduced their production schedules, leading to lower demand for SiMn alloy. Additionally, downstream steel mills faced high production costs, weak end-user steel demand, and rebar spot prices fluctuating downward. Steel mills also experienced prolonged losses, making them cautious in procuring raw material SiMn alloy.

IV. Supply and Demand Aspect:

In 2024, on the supply side, although SiMn alloy production decreased YoY, the severe surplus in 2023, combined with social inventory from 2023, kept SiMn alloy supply at a high level. On the demand side, downstream steel mills reduced production schedules, leading to a decline in SiMn alloy demand. Overall, the oversupply situation for SiMn alloy persisted.

V. Outlook for 2025:

Supply side, SiMn alloy plants in north China are expected to maintain high operating rates due to lower production costs, while plants in south China may adopt more flexible production schedules due to higher costs compared to their northern counterparts. Demand side, SiMn alloy's primary downstream application remains rebar production, and crude steel production in 2025 is expected to decline, reducing demand for SiMn alloy. Regarding spot prices, due to the severe capacity surplus of SiMn alloy and weak downstream steel mill demand, the oversupply situation for SiMn alloy is expected to persist, with spot prices likely to fluctuate downward.

》Subscribe to View SMM Manganese Product Historical Price Trends

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)